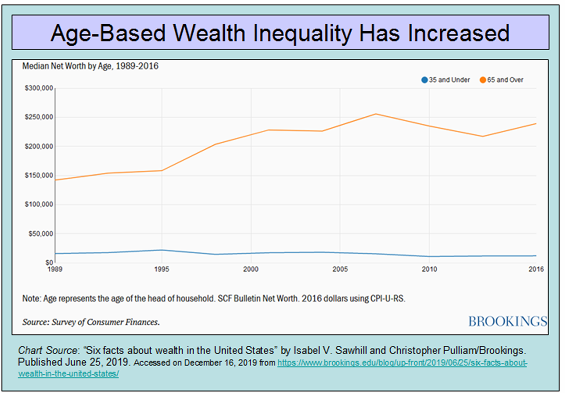

First, documentation that age-based wealth inequality has increased:

Second, to shed light on the matter, document the composition of wealth by Income group:

Okay, don’t get lost in the teeny print. Point is, for most Americans, principal residence is the primary sources of wealth. After that: pensions and retirement accounts. But nobody expects younger adults to have much in the way of pensions or retirement accounts. So the question becomes: why are younger adults delaying home ownership? The next two charts tell a big part of that story:

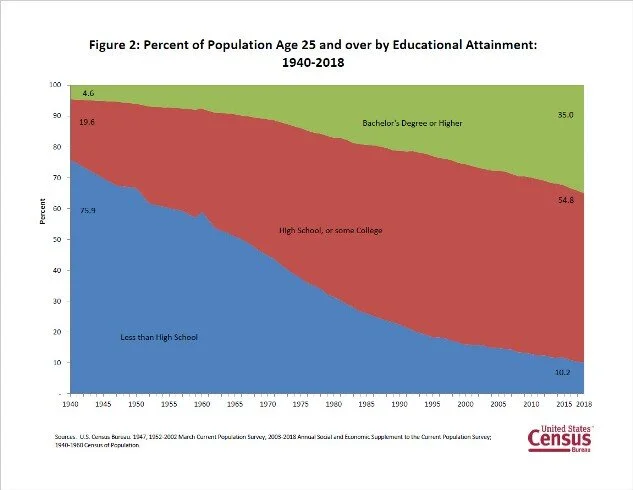

One big reason is later marriage. But why delayed marriage? Partly because of changing cultural norms and partly because more young adults are staying in school longer:

Bottom line: young adults - aka millennials - are in school longer and marry later than earlier generations, so they’re delaying homeownership. Which means they won’t start accumulating wealth in the form of home equity until they’re approaching middle age. Compared to their elders, millennials also have higher levels of student debt, face tighter mortgage lending standards, and tend to live in cities with nonoptimal housing markets. While the late start in wealth-building means a painful period of catch-up, it doesn’t appear to reflect the failure of government or economic system.

References:

“Distribution of Wealth Group Comparisons Distributional Financial Accounts” Federal Reserve Last Update: November 06, 2019

“The Real Reasons Millennials Aren't Buying Homes” by Aaron Hankin/ Investopedia Updated Jun 25, 2019